Dear reader,

This second RO Long Read series is a deep-dive into the Iraqi fintech sector.

This series was written by RO Correspondent Rabel Kaka. Based in Iraq, Rabel is a senior research associate at MAGNiTT and has recently become a fine connoisseur of the Iraqi fintech scene.

He's spent the past few months interviewing Iraqi fintech startups, Iraqi VCs, and other relevant parties to paint a picture of where Iraqi fintech stands today.

Some of the topics Rabel uncovered include:

- The dichotomy between digital commerce and digital transactions (the former doesn't automatically lead to the latter).

- The benefits of digitizing and formalizing the Iraqi economy, and why it has become a governmental priority.

- The Iraqi government's efforts to push digital payments in the public sector.

- The hesitations Iraqi consumers and businesses have vis-a-vis digital payments, and how founders are building with those hesitations in mind.

- The current Iraqi "payment stack".

- Why fintech Iraq is bank-dependent, not bank-disruptive.

- The notable, encouraging evolutions in the Iraqi regulator's posture.

This RO Long Read series comes in at 8,000+ words. We've broken up into two parts. Please find part I below.

Digital commerce doesn’t mean digital payments

Iraq has always been a high-velocity cash economy. People buy, sell, ship, and restock constantly. Cash is the default tool that keeps those transactions moving.

Even during periods of volatility (be it economic turbulence or actual armed conflict), commerce continues. Markets stay open, wholesalers distribute, petrol stations operate, and households spend. Most of that activity runs on cash.

This large consumption-driven economy, operating with limited modern payment rails, is where the Iraqi fintech story begins.

After ISIS was territorially defeated in 2017, daily life began to normalize around the country. As stability improved, digital activity expanded. E-commerce platforms grew, logistics networks became more organized, and social commerce (selling goods through social media platforms such as Facebook and Instagram) became a mainstream way to discover, buy, and sell products.

The more commerce moved online, the more apparent the payment problem became. Browsing and ordering digitally still ended with a cash handoff (a process known as “cash-on-delivery”, aka “COD”).

Mohammed Jamal founded KAPITA Research, a Baghdad-based market intelligence firm that maps Iraq’s digital economy. He explains that Iraqis had initial exposure to what could be considered “pre-fintech” products long before digital banking products became available. Iraqis were already interacting with “digital value” through everyday instruments such as telecom recharge cards, online vouchers, and prepaid Visa or Mastercards.

These tools were often used to pay for goods or services that could be purchased through digital payments, such as App Store subscriptions, software licenses, online gaming credits, or even goods from international e-commerce platforms. While these tools didn’t equate to financial inclusion per se, they gradually trained consumers to interact with digital balances and digital verification.

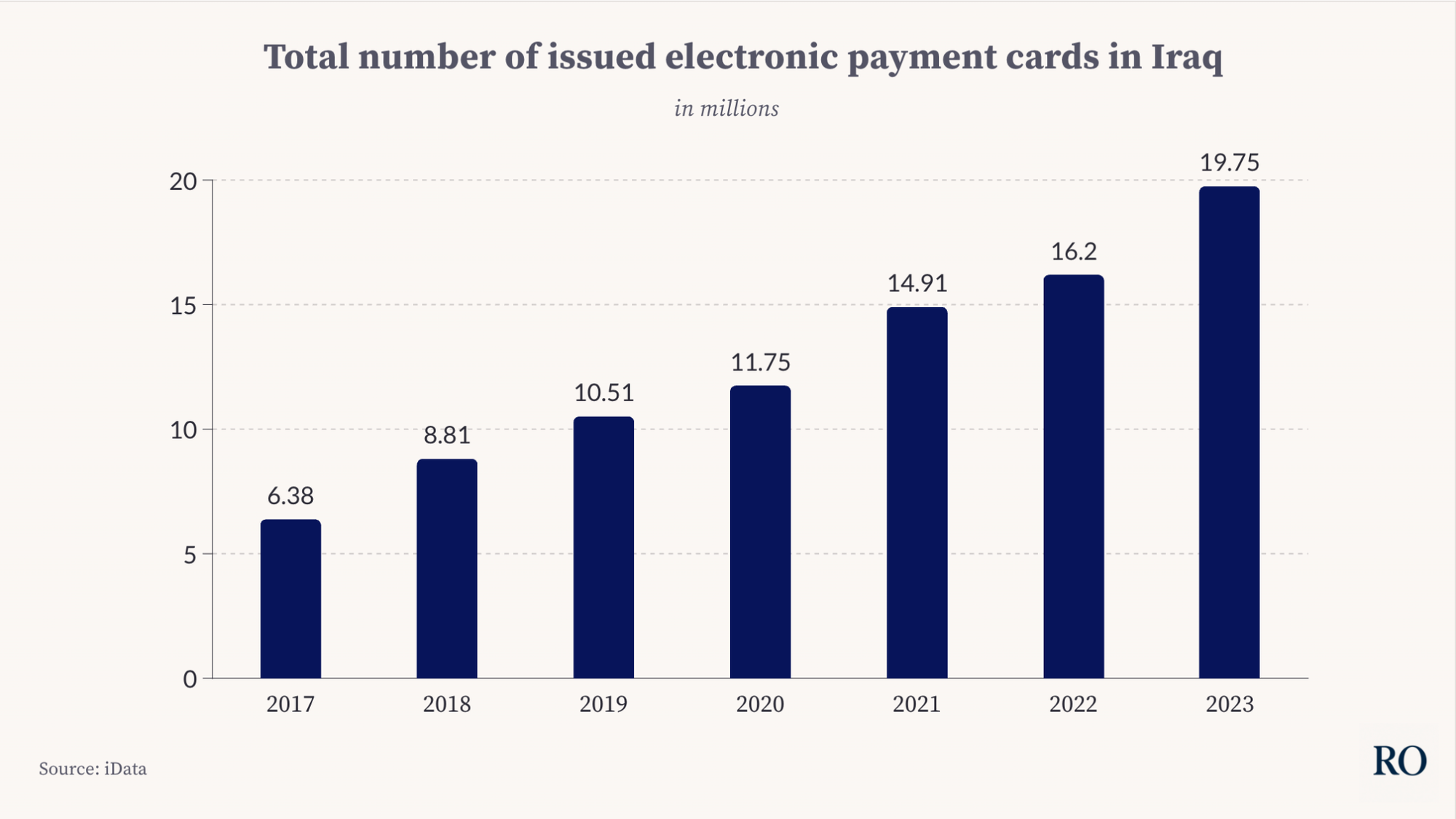

2017 marked an inflection point. The Iraqi government and the Central Bank of Iraq (CBI) launched a nation-wide transition of its public payroll system from cash payments to electronic, bank-issued cards. That decision brought mass exposure to digital balances for millions of Iraqis, many of whom were interacting with ATMs and point-of-sale (POS) infrastructure for the first time.

In practice, these “salary cards” are debit-style cards linked to bank accounts, allowing employees to withdraw wages or pay electronically rather than collecting envelopes of cash. The policy was partly driven by concerns about transparency and leakages in public payroll systems. Moving salary payments into bank accounts allowed the government to track disbursements more accurately while also expanding the formal financial system.

Source: iData

As salary payments moved onto bank accounts and cards, more government services began requiring digital payment for administrative fees. POS terminals became increasingly common in major cities. In 2025, the Iraqi government reported that all official government institutions had implemented electronic systems for payments and revenue collection, forming part of a broader public-sector digital transformation strategy.

Mustafa Sirri, a financial sector advisor with deep experience in Iraq’s banking and payments ecosystem, noted an early example of this impetus: the deployment of POS terminals at Baghdad fuel stations at the start of 2024. This initiative was encouraged by the CBI and participating payment operators as a normalization tactic to broaden exposure to digital payment acceptance, even when public comfort with these tools was still emerging. The CBI has supported targeted campaigns to expand POS use in public contexts, such as deploying devices in public transport vehicles and taxis in Basra under the National Financial Inclusion Strategy (NFIS) 2025–2029.

These efforts paid off (although we’ll later discuss the caveats of such government mandates). Digital transactions in Iraq skyrocketed over the past few years. A KAPITA study found that electronic transaction volumes grew from roughly 1 million in 2018 to 11 million by 2023. However, the same study shows that in several sectors, including e-commerce and ride-hailing, digital payments still accounted for less than 10% of transactions. More transactions are happening digitally, but cash still underpins most of them.

The CBI’s NFIS report confirms this reality. It reports that 95% of Iraqis use cash for all expenses, and 97% withdraw their entire salary or benefits in cash even when received digitally. That means salary cards often function as cash-out tools rather than everyday spending accounts.

This is not because Iraqis do not understand the digital realm. Mohammed Jamal from KAPITA framed the core constraints as trust and incentives. Many households learned over decades that cash is safer than institutions, because institutions can fail, freeze, delay, or change rules overnight. For instance in July 2023, following a sudden U.S. regulatory crackdown, the Central Bank of Iraq abruptly halted all U.S. dollar cash withdrawals, leaving many depositors unable to withdraw their dollar balances and forcing them to convert into Iraqi dinars at the official rate, roughly 15% below the parallel market rate. When the “safe” option is cash, digital transactions need strong arguments to win.

Saif Aljaibeji, founder & general partner at Urth ($50M Iraqi growth stage fund), describes the same constraint from an operational perspective. Both merchants and consumers need to trust that the system will work before shifting away from cash. Merchants must feel confident that digital gateways will reliably settle their balances, while customers must trust that the institutions processing those payments will protect their funds. As long as both actors don’t trust the underlying digital payment system, cash remains the default.

The cost of cash

For the government, cash dominance creates practical problems. It reduces visibility over economic flows, limits formalization, and weakens financial integrity controls. That is why the NFIS frames digital usage and account ownership as development priorities rather than optional upgrades.

For businesses, especially SMEs, digital payments solve a different problem: proof of revenue. The IFC estimates Iraq has about 608,500 SMEs and an SME financing gap of about $6 billion. In a cash economy, revenue is hard to verify, so credit becomes expensive or unavailable. Banks are understandably reluctant to lend to a business they have little verified revenue information about. Digital transaction records create an auditable trail, and that trail becomes the starting point for credit underwriting.

This disconnect between economic activity and financial digitization is precisely why fintech matters. Iraqis already browse, purchase, and sell products online. What remains underdeveloped is the conversion of that activity into digital transactions. The market for Iraqi fintech products exists but is still dormant. Aligning incentives, providing compelling use cases, and building trust is what Iraqi fintechs need to wake up their prospective customer base.

Quantifying said market

Iraq’s size amplifies the importance of that alignment.

The country’s population reached approximately 46 million in 2024. More than 60% of the population is of working age (15–64), while roughly 36% is under 15. Iraq’s GDP stood at roughly $279.6 billion in 2024, with GDP per capita at $6,074.

Final consumption expenditure increased from $126.86 billion in 2017 to $172 billion in 2024, according to World Bank data. This expansion reflects a gradual return of domestic economic activity following several years of improved stabilisation and security conditions after 2017. These figures also reflect a substantial domestic market for digital payments. When most transactions in an economy of this size remain cash-dominant, inefficiencies accumulate across millions of daily exchanges.

IraqiNews reported that the World Bank expects Iraq’s economy to record the highest growth rate among Arab countries in 2026, reaching 6.7%. The report notes that this is driven by a rebound in the energy sector and rising oil exports, alongside government measures to expand infrastructure expenditure and diversify revenue streams. However, this outlook remains sensitive to geopolitical developments, as disruptions to oil exports through the Strait of Hormuz have already constrained Iraq’s production and export capacity.

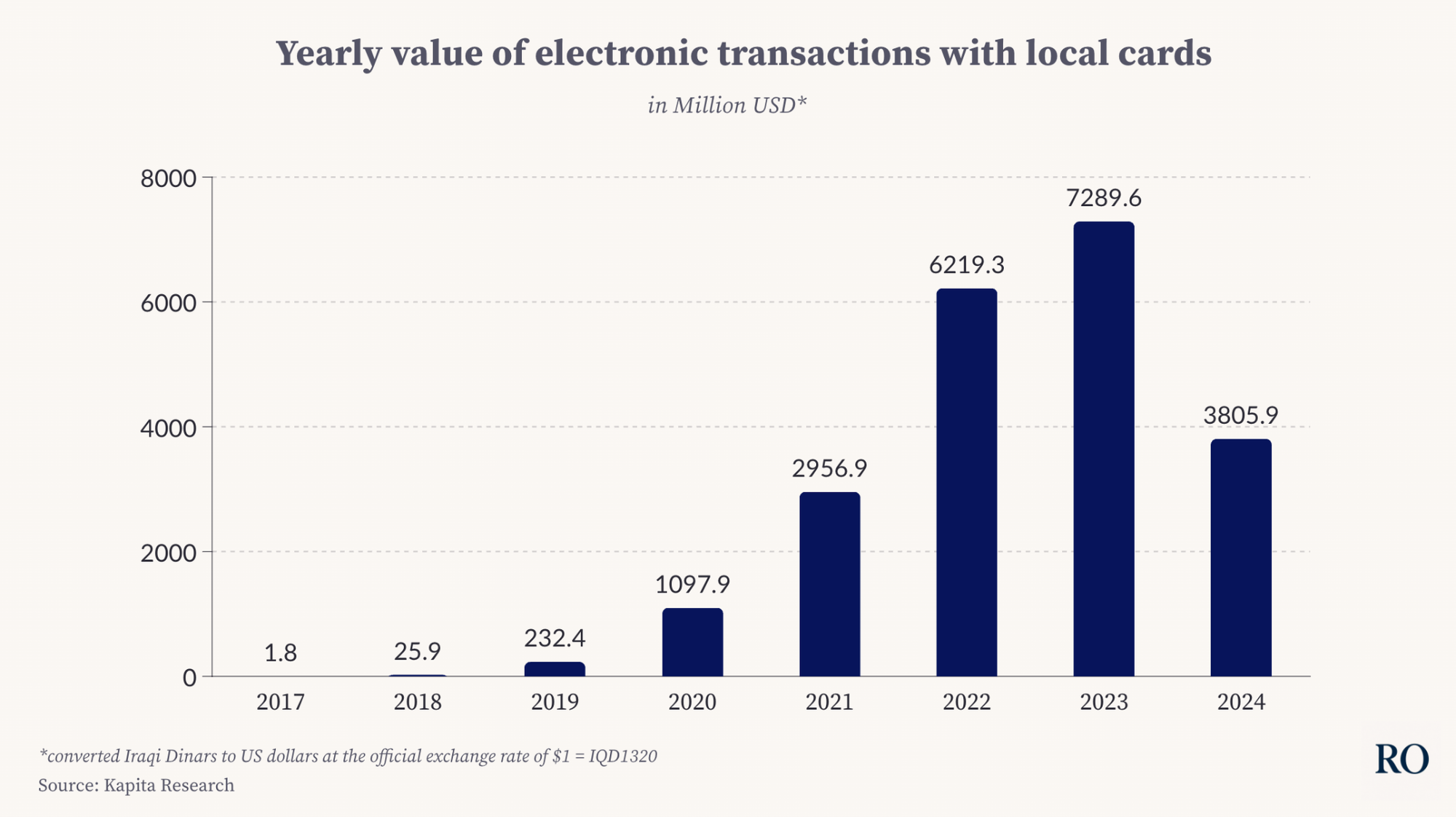

This broader economic growth has been reflected in Iraqis’ use of digital payments, as the graph below shows.

Source: Kapita Research, Does Iraq Have a Digital Economy?, p. 70, available here.

Note: The decline in 2024 likely reflects tighter regulation on cross-border card usage and U.S. dollar transactions introduced in 2024. This reduced arbitrage-driven activity linked to the gap between official and parallel exchange rates.

A distinct Iraqi advantage (compared to socio-economically similar markets) is that connectivity and access to digital smartphones is widespread. According to Digital 2024: Iraq recorded 36.22 million internet users at the beginning of 2024, implying penetration of 78.7%. Smartphone adoption is widespread in urban centers, particularly among younger demographics. The tools necessary to conduct digital payments are widely available to the Iraqi masses.

Revand Bamarni, an investor at Meso Capital (an Iraqi investment firm), sees Iraq’s widespread smartphone use, internet access, and improving financial rails as signs that many of the foundations for digital banking are already in place. In his view, the combination of local demand, regulatory progress (discussed later in this article), and internationally-led banking reforms are beginning to align. This makes the next phase of digital banking growth increasingly achievable.

Revand also points out that financial services still account for a very small amount of Iraq’s GDP, materially lower than in comparable emerging markets. This belies how much room remains for banking, payments, lending, and insurance services to grow as more transaction activity moves into the formal financial system.

Yet, the shift from readiness to adoption depends on one missing layer: broader participation in said formal financial system.

The bottleneck lies in bank account ownership. The NFIS shows how early Iraq still is in that journey; it reports that only 11% of the population currently owns a bank account, with a national target of reaching 50% by 2030. When you combine low bank account ownership with high cash usage, you get a market where commerce exists but the institutional financial system captures only a small share of the transaction flow.

RO Insights: the compounding benefits of financial formalization

Financial formalization, for both individuals and businesses, leads to auditable financial trails. Confidentiality concerns are legitimate (the crypto movement originated from them, in part) but these auditable trails can lead to immense benefits.

Take India, which is a few years/decades ahead of Iraq in its fintech journey.

QuickLend, an Indian fintech startup, realized that the number of Indian retail investors was growing. One can assume that upstream, the growth of Indian retail investors came from first bank account ownership, then a desire to invest the assets held in those bank accounts.

QuickLend enables these retail investors to pledge the financial assets they own, such as mutual funds, as collateral to unlock loans. These loans are safer than loans without collateral (ie: unsecured loans)l, which come with colossally high interest rates and can plunge people into distressing debt.

Here’s how Raghuram Trikutam, one of QuickLend’s co-founders, explains the main use cases for his product:

“We don’t have a definite borrower persona. But we have an ideal ticket size based on the loan amount, around INR 250,000 (~$3,000), which is significantly higher than the ticket size for unsecured loans, which is in the range of INR 50,000 to 75,000 ($550 to $875).

However, we also support high-ticket loans; the largest sum we serviced was a loan of INR 20 million ($230,000). We don’t support loans below INR 25,000 ($300). This naturally filters the borrower base. Our pledged AUM right now stands at INR 72 million ($850,000).

Most of our borrowers have been investing INR 5,000 to 10,000 ($58 to $120) a month in the markets through mutual funds for a couple of years. They’re usually earning at least INR 600,000 ($7,000) per annum, and they want to preserve their long, drawn-out investments while accessing cheaper capital.

In terms of our customers’ use cases, we’ve seen a wide variety. One borrower took a loan to make a down payment on a plot of land, something traditional home loans don’t cover. Someone else used the loan to fund his daughter’s wedding. There’s no single use case.

On the business side, we’ve seen that working capital financing is a recurring reason. Our key value proposition (as opposed to SME loans from banks and NBFCs) is speed and cost.

SME loans take one to two weeks and come with interest rates between 12% to 25%. If you have mutual funds, we can disburse the loan within an hour, at 10.5%. It’s fully digital, and the process is simple. It’s important to note that in this case, the business owner takes a loan against their personal mutual fund assets, and uses the loan as operating expenditure (OPEX) for their business. It’s not a popular mechanism yet.”

Excerpt from QuickLend: safer B2C lending in India, originally published in The Realistic Optimist (June 2025)

The Iraqi fintech market

Iraq is often described as an early-stage fintech market, implying immaturity or absence of demand. That framing is incomplete. The demand is already there. The gap, as we’ve explained, is that digital payment infrastructure hasn't caught up with how Iraqis buy and sell.

Simma is a useful example, because it started as a workaround for a broken cross-border payment reality. Co-founded by Samer Tarazi, Simma is an Iraqi e-commerce and fintech company that enables Iraqi consumers to purchase from international brands while using local payment methods.

Prior to Simma, Ghassan Saad, the company’s other co-founder, ran a one-person dropshipping operation. He served Iraqi customers who couldn’t buy from platforms such as Amazon, Ikea, or Shein due to international banking restrictions on their local Iraqi cards. Customers sent Ghassan product links, he purchased them using a foreign credit card, and they paid him locally. Despite operating alone, he claims the business generated over $1 million in GMV. That model was obviously unscalable, but it was clear proof that Iraqi consumers were seeking access to global commerce and were willing to pay for a bridge.

Samer convinced Ghassan to productize what he was already doing, a process that eventually became Simma. Their MVP was deliberately simple. They ran paid ads on Facebook and Instagram telling Iraqis they could order from Shein and receive delivery at home, in Iraq. Over six weeks, with only $350 spent on ads, the platform generated more than $130,000 in orders. The response was strong because the consumer demand already existed, but the infrastructure was missing. It was a signal of deprivation.

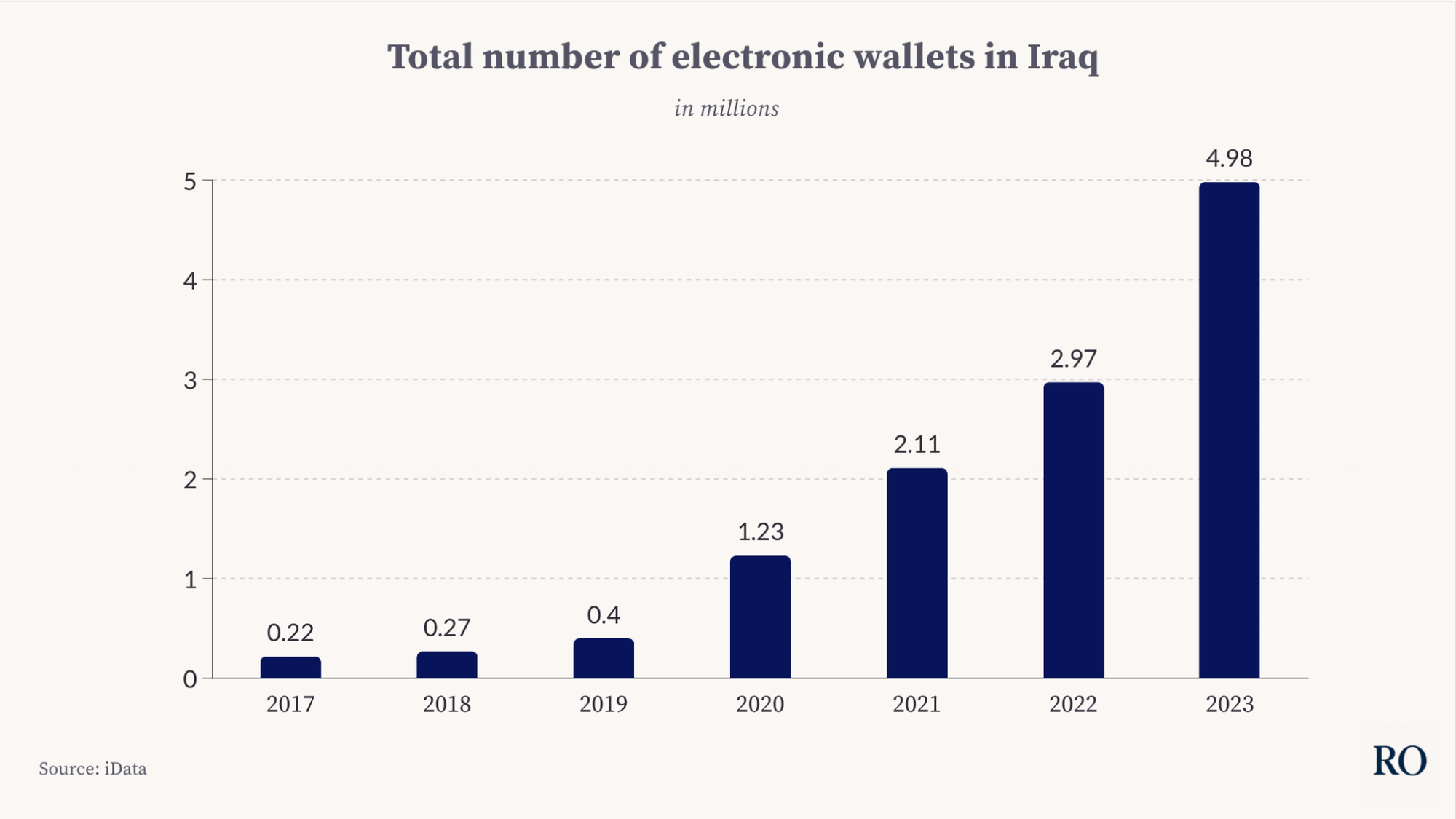

Simma’s internal wallet data points in the same direction. According to the company, average order value on wallet transactions reached $210, materially higher than typical regional e-commerce averages. Samer also noted that 17% of Simma’s aggregate transaction value has now been settled through the wallet, equivalent to more than $3 million paid digitally.

For a market still overwhelmingly shaped by cash, these numbers signal purchasing power and willingness to transact digitally when the option to do so is available and reliable.

Source: iData

Wayl shows the same pattern but from another perspective: the Iraqi merchant’s. Wayl, founded by Ali Ismail, serves hundreds of thousands of small and medium retailers who operate informal storefronts and sell primarily through social commerce pages (Facebook, Instagram…).

Many of these merchants cannot integrate with regulated payment processors. As Ali explained to The Realistic Optimist, formal business registration costs approximately $10,000, and registration is often a prerequisite to integrating such payment processors. As a result, most merchants rely on cash-on-delivery, even when the sale itself originates online through social media platforms.

Wayl’s proposition is practical. It lets merchants accept digital payments without requiring a formal business registration. Wayl doesn’t bypass the regulated system. Instead, it connects to licensed acquirers itself, then gives informal merchants a way to use that infrastructure through its own checkout and settlement layer.

In practice, this means a merchant who is selling through Instagram or Facebook does not need to become a fully registered business and sign separate contracts with multiple payment providers before accepting digital payments. The merchant plugs into Wayl’s system, while Wayl handles the upstream integration with regulated payment partners. Ali describes the model as a way of turning a fragmented, bank-grade onboarding process into one contract, one integration, and one settlement relationship for merchants who would otherwise remain cash-only.

The company’s GMV trajectory shows what happens when this bridge exists. Wayl processed its first 1 billion IQD (~$767,000 USD) in GMV over 22 months. The second billion took five months. The third took two months. That acceleration suggests that Iraqi merchants aren’t resisting digital payments, but rather adopt them quickly when the infrastructure is simple, accessible, and usable within the realities of informal retail.

Simma and Wayl point to the same conclusion. Iraq’s fintech opportunity implies building rails that convert existing commerce into digital flows, at scale. The demand is there, both from consumers and merchants.

The floodgates ought to be opened.

Part II of this RO Long Read has been published here.

Disclaimer: we have done our absolute best to verify the veracity of all facts we mention. Some facts are more subjective than others and thus prone to dispute. If you find errors, please email tim@realisticoptimist.io