Dear reader,

Except in frontier tech scenarios (ie: nuclear fusion), building the tech is rarely the hard part. What's difficult is acquiring and retaining customers.

A trite piece of advice is that doing so requires understanding customers' pain points. That advice is correct, but incomplete. Real insights comes not only understanding those pain points, but also ranking them.

A cash-strapped startup might only have the resources to solve one of the pain points it identifies. Defining the most salient one and going after it is key to the startup's immediate commercial relevance, and ultimately its survival.

Repeat founders might have an advantage in this. Especially if they keep founding companies in the same sector. Their granular understanding (and ranking) of customers' pain points is refined by years of operational grind.

That's the case for the company we cover today, Smartlane.

Smartlane is a Pakistani startup founded by three repeat founders: two in e-commerce, one in fintech. Unsurprisingly, Smartlane combines both expertises by offering logistics and financing solutions to Pakistan's e-commerce merchants. So far, they've onboarded 1200 merchants and have extended $28M in credit.

The Realistic Optimist's exclusive 2,500+ word interview with the founders covers:

1) How their Pakistani e-commerce experience helps them prioritize merchants' pain points (ie: starting with courier aggregation, not financing).

2) Their product journey from MVP to the three-pronged revenue stream they sport today.

3) A deep-dive into their cash-on-delivery (COD) settlement product, and the financing mechanisms undergirding it.

4) How Pakistan's instant payment system, Raast, impacts COD's relevance in the e-commerce landscape (ie: less than you think).

5) Operational challenges with their courier aggregation model.

6) Their international expansion strategy.

7) Best and worst strategic decisions so far.

8) Common pushbacks they get from VCs (and their response to them).

... and more.

Biography

Fatin Tariq Gondal, Adam Ghaznavi and Umer Munawar are the co-founders of Smartlane, a Pakistani startup providing logistics and finance solutions for Pakistan’s e-commerce merchants.

Smartlane has onboarded over 1200 merchants, works with 24 local couriers, and has extended over $28M+ in credit. The company has raised $2.3M in funding.

Prior to Smartlane, Fatin and Adam co-founded WebWorks, an e-commerce management agency. Fatin has prior experience at Rocket Internet, while Adam has prior experience at Careem. Umer has a finance background, previously co-founding Finja, a Pakistani fintech.

You have extensive experience in Pakistani e-commerce. What do you understand that other founders in this space don’t?

We have an accurate, lived understanding of what Pakistani merchants’ pains are. More importantly, the “priority level” of these pains.

We knew courier aggregation had to be the first product we built, well before even thinking about financing or becoming a courier ourselves. Pakistan’s courier ecosystem is deeply fragmented and heavily saturated. Merchants don’t rely on a single courier; they’re forced to work with multiple providers to balance coverage, performance, and cost.

Managing that complexity is a pain. Instead of adding yet another courier to an already crowded market, we chose to build a system that sits above the ecosystem, unifying it and solving the real operational and financial pain points merchants face every day.

What did your MVP look like?

Merchants were working with multiple couriers, tracking and reconciling package deliveries through different portals… We built a centralized dashboard for them to manage and track all of their courier operations from a single place. Then, we layered on financing products.

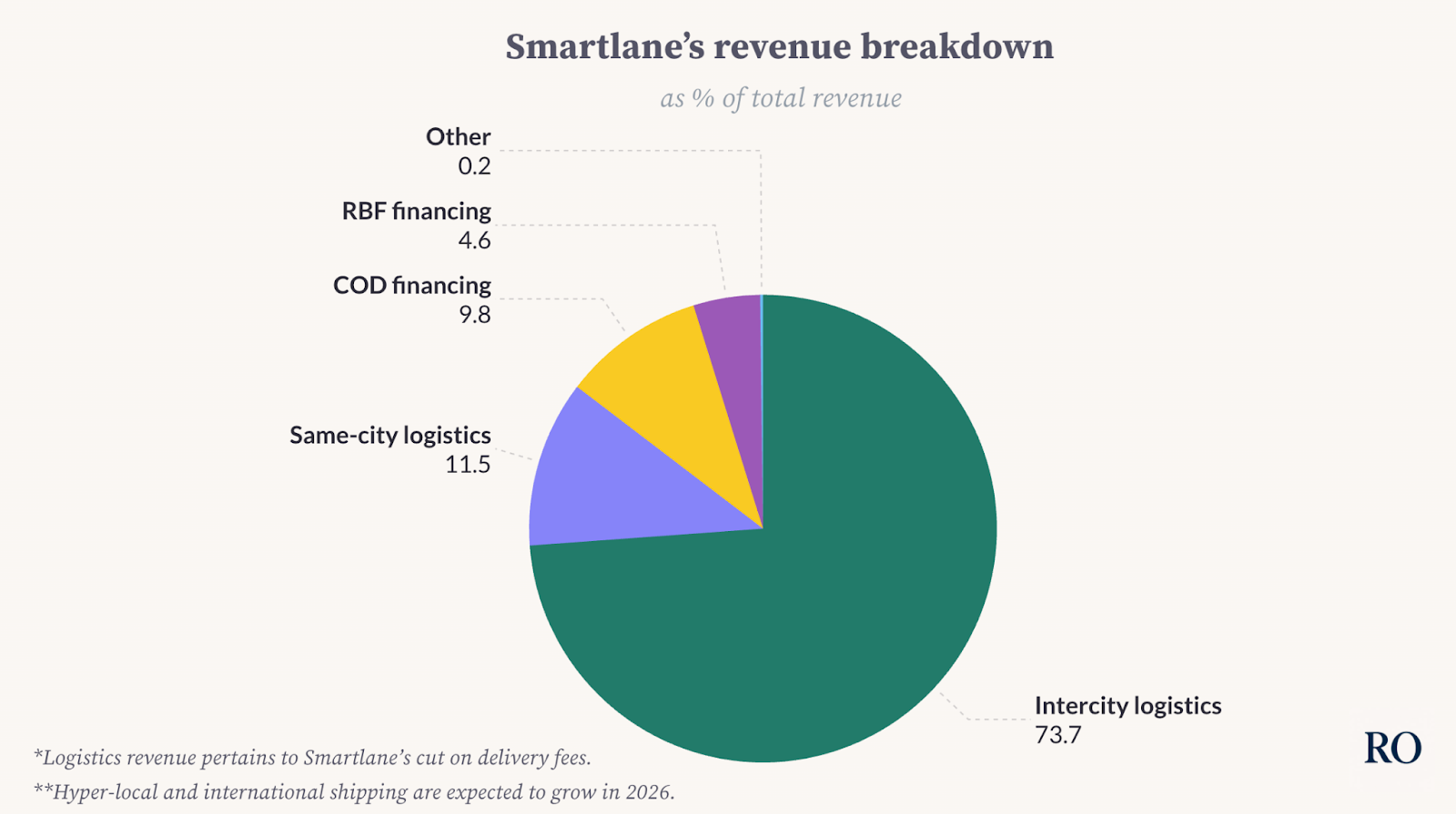

What are your main products today?

The first is our SaaS platform. When an order lands on Smartlane, we push it to the best performing courier on that delivery route. This optimises delivery timelines, thereby reducing returns and cancellations (late, poorly-serviced deliveries increase returns/cancellations). The merchants manage their orders and deliveries across multiple couriers from a single place. We take a cut on delivery fees that transit through our SaaS.

The second is our cash-on-delivery (COD) settlement product. Here, we pay merchants 80% of the order’s delivery value upon shipping, avoiding merchants the hassle of waiting for the courier company to circle back with the money. We then collect payment from the courier company ourselves.

Third is our revenue-based-financing (RBF) product, where we provide merchants with short tenure growth capital loans. We have excellent underwriting data since we centralize all of a merchant’s transactions.

Source: Smartlane

What does your client base look like?

We’re focused on small and mid-size merchants. Enterprise merchants generally enjoy preferential delivery rates and payment reconciliation terms with couriers, thanks to their high transaction volume.

Small and mid-size merchants don’t. We unlock those preferential rates and terms for them, since our aggregation model creates the volume couriers need to extend such discounts.

As of today, a sizable portion of our merchants work in the women's fashion & beauty sector, followed by electronics, home accessories, and kids items.

Our average merchant sells between $7,000-$8,000 of goods per month, with a basket size between $10 and $15.

How do you finance the COD settlement product, on your end?

Through a dedicated lending fund structured with a non-bank financial institution (NBFI) partner. The fund is capitalized 50/50: Smartlane contributes half from its balance sheet, and the NBFI contributes the other half. This creates immediate lending capacity without requiring Smartlane to hold a lending license or build a deposit-funded model.

The NBFI serves as the fund’s administrator, underwriter, and investment-banking partner. Underwriting is fully digital: Smartlane transmits merchant performance and repayment signals to the NBFI in real time, the NBFI completes credit approval, and funds are then disbursed directly into Smartlane’s closed-loop wallet.

Repayments are recovered automatically from COD proceeds. When couriers remit COD collections (ie: couriers sending Smartlane the cash it recuperated from a COD order), Smartlane routes the agreed installment to the debt fund’s account. This keeps the repayment mechanism operationally simple and tightly controlled.

On that COD settlement product, how long is the loan “outstanding” for?

On our COD settlement product, the loan is typically outstanding for around six days—that is the effective duration of the portfolio. This timeframe is when merchants need a liquidity injection the most, which our COD settlement product provides.

This creates an intrinsic incentive for us to optimize couriers’ routes. The shorter the timeframe between delivery and payment reconciliation, the shorter time the loan is outstanding for. The faster we get paid back, the faster we can issue another loan.

Historically, merchants often waited up to 30 days to receive COD remittances from couriers, largely because they lacked the volume concentration and contractual enforcement mechanisms that Smartlane brings to the table. Our COD settlement product flips the script.

How do you manage returns, if you’ve already wired the merchant the COD settlement amount?

We manage returns through a combination of risk-based advance sizing and automatic netting.

Before advancing funds, we estimate a merchant’s expected return rate using their historical performance and sector-level return benchmarks. That informs the advance rate—which is typically up to ~80% of order value—so the product is structurally resilient to routine returns.

Operationally, if a shipment is returned after we’ve advanced the merchant, we don’t treat it as a separate collection problem. We recoup the amount by netting it from the merchant’s next COD settlement cycle. Because we only finance up to ~80%, there is an embedded buffer that absorbs normal return volatility.

RO Insights: securitizing a loan book

A way to scale a loan product is to securitize the loan book. In other words: bundle up the loans into a financial product that can be sold. The buyer of the securitized loan book becomes a recipient of the loan repayment.

This enables the company to scale its lending faster, as it doesn’t hold the loans on its balance sheet anymore.

Here’s how Sebastian Kreis, co-founder of Chilean startup Xepelin (which extends loans to SMEs) explains:

“We could theoretically hold the loans we extend as an asset on our balance sheet. That would weigh us down, as we’d be limited by the money we have on hand to extend more loans. It also means all of the risk is on us.

What we do instead is wrap up those loans into SPVs. Investors can invest in those SPVs, and become entitled to a share of loan repayments. We thus access instant liquidity from the SPVs we emit, and shift part of the risk to the SPV’s investors rather than us directly.

That structure enables us to scale the loan volume we extend much faster. We have around 15 of these SPVs today. Those SPVs are also a great way to create initial relationships with potential debt issuers.”

Excerpt from Xepelin: raising $300M to finance LATAM’s SMEs, originally published in The Realistic Optimist

Do you securitize your loan book?

Not yet. That’s the Holy Grail in terms of scaling a loan product. We’re in the first phase of securitization if you will.

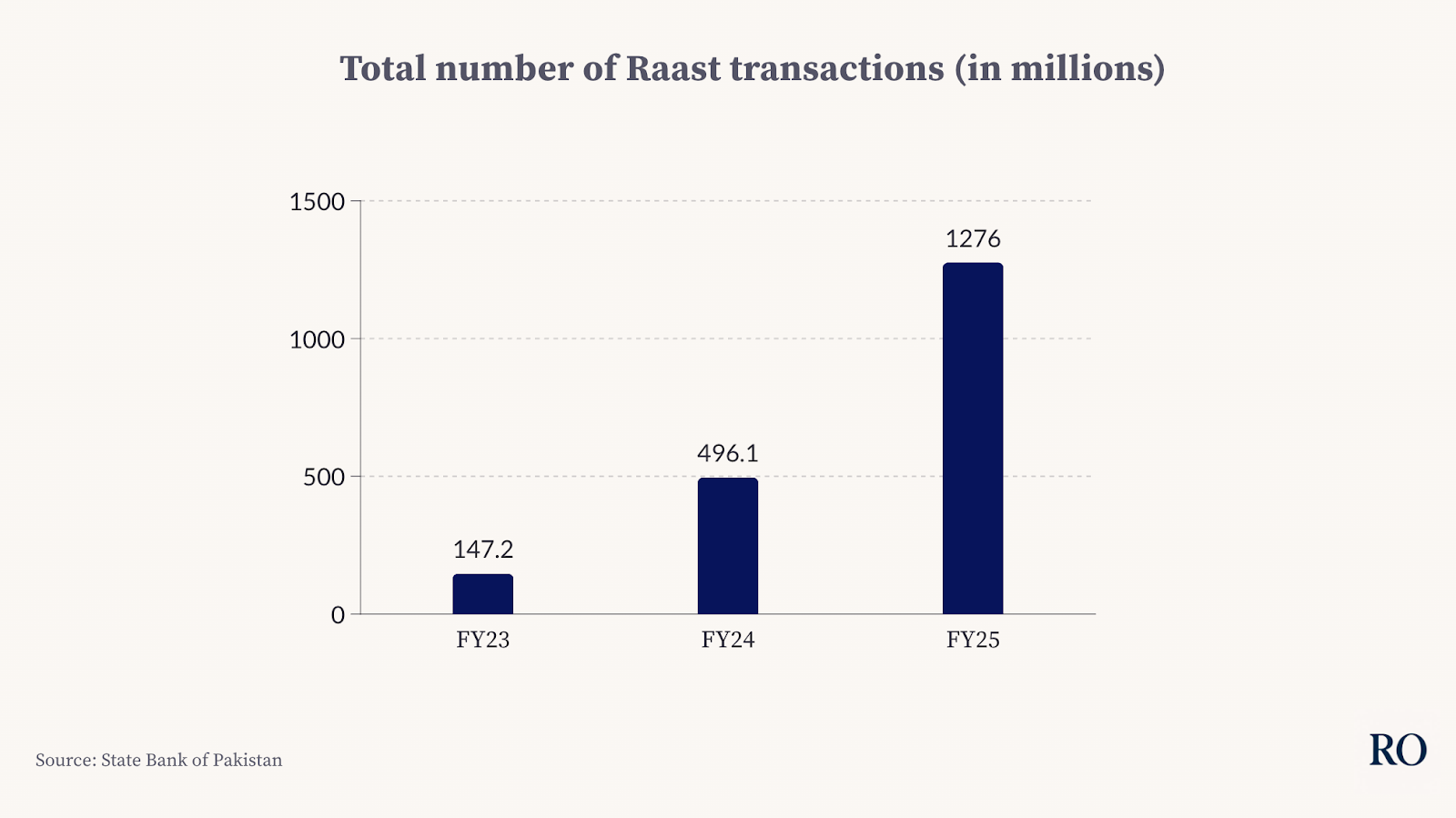

Raast (Pakistan’s digital instant payment system) is growing. This means COD will lose relevance. How did you factor this into your strategy?

We’ve built the strategy assuming COD declines slowly, not overnight. Even in India—despite aggressive digitization—cash-on-delivery has remained a major share of e-commerce (~65% of orders), largely because trust is built at the point of delivery.

Our core bet is that the first real shift happens at the doorstep: the courier rider stops collecting cash and instead collects digitally (QR/instant transfer). In that world, we’re still solving the same problem (accelerating settlement and working capital) but the receivable moves from “cash remitted later” to “digital funds collected instantly.” That shortens the outstanding period, improves reconciliation, and lets us recycle capital faster.

Today, over 80% of the e-commerce orders that transit through us are paid via COD. We have time to plan for its demise.

Source: State Bank of Pakistan

How come Raast is growing while e-commerce remains doggedly tied to COD? Where is Raast used then?

Raast is mostly used for P2P payments, bill payments, and salaries. Corporates use it. Small merchants such as grocery stores, petrol stations, and pharmacies are also increasingly integrating Raast into its checkout flows (alongside other digital wallets, like JazzCash).

E-commerce, meanwhile, stays tied to COD because “COD” represents pay-on-receipt trust at the doorstep (inspection, returns, fraud risk). Raast’s next wave is merchant payments, so the likely transition is cash at the doorstep to digital at the doorstep, not an immediate shift to prepaid orders.

What are your thorniest operational challenges?

First, we’re merchants’ single point of contact but we don’t actually run the deliveries. We don’t have control over a courier messing up but we’ll get the blame for the mistakes. That can be frustrating.

The Pakistani courier market is so competitive that many couriers invest in subsidizing delivery fees to gain market share rather than improving their customer service infrastructure. It’s hard to convince couriers to invest in better service, even though we’re the ones liable for that service in merchants’ eyes.

Second, Pakistan still suffers from paltry address infrastructure. It can be hard to find someone’s house. This is an industry-wide challenge though.

Third, we aggregate 20+ couriers but each operate on their own standards. There’s no common SLAs. Every courier has their peculiarities, their own tech stack… We’re trying to streamline some operating procedures with the newer, younger courier companies.

RO Insights: digital maps for emerging markets

Lackluster address systems are a common complaint by founders in emerging markets.

Here’s how Tayef Sarker, co-founder of Bangladeshi startup Barikoi (which builds digital maps for emerging markets), explains the root issues:

“Google adequately invests in markets they know will be lucrative. Bangladesh neighbors India (a larger, more affluent market), where Google obviously preferred to spend more resources.

Building reliable maps for Bangladesh required significant investments because a company like Google can’t apply a Western lens here. Addresses aren’t organized through names, they are situated in relation to a specific “landmark” (ex: the house is “just behind the big tree”). In the US, the government publishes useful data for map makers. Not so much in Bangladesh. The granular, data collection work has to be done from scratch, by hand.”

Excerpt from Barikoi: accurate maps for emerging markets, originally published in The Realistic Optimist.

In light of those challenges, aren’t you tempted to build your own courier fleet?

No. We don’t want to “own” the package. We want to serve merchants by efficiently aggregating the most relevant couriers for their deliveries. What we could imagine in the future though is adding services for couriers. This can include a warehouse for multi-point dispatch, mPOS…

What does expansion mean for Smartlane?

We’re currently focused on replicating the Smartlane experience for international transactions. We want to make it easy for Pakistani merchants to sell and ship items abroad.

There’s a ton of demand on the Pakistan-UK, Pakistan-US, and Pakistan-GCC corridor. That demand stems from Pakistanis in the diaspora buying Pakistani lifestyle products (cosmetics, oils, clothes). The Pakistan-GCC corridor is doubly-important because orders from India (mostly designer retail) go through there, since there are no India-Pakistan deliveries (ED: due to geopolitical tensions). For obvious reasons, no official statistics exist on this corridor but we believe we can drive $1B in India-Pakistan orders in 2026.

It’s a nightmare for a Pakistani merchant to ship items abroad. Enabling them to do so yields a huge, untapped market. The flip side of that coin is that we need to build everything from scratch.

We’re running pilots with two couriers (Leopards and TCS) to set-up the relevant tech (APIs for cross-border logistics) as well as establishing legal entities and partnerships in the markets we want to deliver to.

What’s been your biggest strategic mistake?

Our biggest strategic mistake was building the early business around a small number of large merchants and long-tenor financing, instead of designing for breadth and repeatability from the start.

That approach delivered fast initial growth, but it came with structural fragilities: a concentrated portfolio (churn hurt disproportionately), merchant bargaining power that compressed margins, and a model that required a constant supply of liquidity to keep scaling.

What about the best decision?

Focusing on serving smaller merchants rather than enterprise ones is more cumbersome but more rewarding. We’re really solving problems for these merchants, which not only feels good but also means these customers are stickier.

We also did a decent job of not playing the “subsidizing delivery fees to unlock growth” game. This kept our unit economics sane.

What foreign proxy is Smartlane most modeled after?

ShipRocket in India.

What’s the most common investor pushback you get and how do you respond?

A lot of local VCs didn’t understand the market as well as we did. Most spoke to a couple of merchants and thought they’d mapped their pain points. As a result, many backed “tech-enabled” couriers that now compete in a race to the bottom on delivery fees. Our aggregation approach didn’t make sense to them.

That left foreign VCs, most of whom are wary of Pakistan as a market. We’ve gotten three term sheets pulled from under our feet because of Pakistani political events (chief among them the arrest and imprisonment of Imran Khan, Pakistan’s former PM, on May 9th, 2023).

In hindsight, a dry fundraising environment forced us to develop a sane business, unit-economic-wise. Maybe that wouldn’t have been the case if we’d raised a ton of money during the heady 2021 days.

RO Insights: local capital, an antidote to international markets' tantrums

Having a robust pool of local capital investing in local startups is key for ecosystem resilience. An ecosystem’s financing shouldn’t be dependent on foreign investors, whose interest is often dictated by the ebbs and flows of interest rates.

Here’s how Ammar Naveed, co-founder of Pakistani social commerce startup DealCart, explains what he believes the Pakistani ecosystem needs to scale:

“It needs local capital. Traditional business owners need to start investing in this space. If you look at other markets such as India and the Middle East, you see a lot of local businessmen investing in startups. In Pakistan, that hasn't been the case yet (at least at a scale that is required for the ecosystem to take off).

One of the key areas where both the government and private sector are making progress is in promoting digital payments. Pakistan's digital payment ecosystem has grown significantly, with transactions surging by 35% in FY24.

That said, we face infrastructure challenges similar to other developing countries. Events like internet outages not only disrupt operations but also negatively impact country branding and customer trust. The government is working on multiple initiatives, including adding additional bandwidth to improve internet speeds in the country.

It seems almost inevitable for a country with a population of 250 million to become increasingly digitized and produce large-scale, consumer-tech businesses. As e-commerce penetration grows rapidly, the ecosystem presents significant opportunities for entrepreneurs and investors alike. It remains one of the largest untapped consumer markets, waiting to be disrupted.”

Excerpt from DealCart: social commerce in Pakistan, originally published in The Realistic Optimist

Is there something I should’ve asked which I didn’t?

There are two topics we’re currently interested in.

First, we want to figure out how to institutionalize Pakistani family offices’ (FO) involvement in the Pakistani startup scene. Central Asian FOs are plowing money into their local ecosystems, but it feels like Pakistani FOs are more timid in that aspect (ED: one source estimates that 1% of Pakistani FOs available liquid investment capital goes into local startup investments).

Second, we’re curious to see what comes out of Pakistani startups moving to the GCC. Many foreign investors have pushed Pakistani founders to expand to the UAE, Saudi… We haven’t opted for that route. We believe there’s a big business to build from and in Pakistan. E-commerce in Pakistan is an industry that keeps growing, year-after-year, despite political vicissitudes. We’re long on it.

Disclaimer: all internal company metrics shared in this article are claims from the interviewee. They have not been independently verified. Do your own due diligence.

The Realistic Optimist’s work is provided for informational purposes only and should not be construed as legal, business, investment, or tax advice.