Biography

Ahsan Jamil is the managing general partner of sAi, a Pakistani VC fund launched in 2022. sAI has the particularity of having raised its fund in local currency (Pakistani rupee) rather than in more traditional $USD. Ahsan previously held executive positions in Fortune 500 companies in the US.

Raising venture debt in local currency seems increasingly commonplace. But raising a VC fund in local currency seems new. Why do it?

It’s very simple. Investing $USD into startups making revenue in Pakistani rupee makes for a tough equation. If the rupee depreciates, the startup’s corresponding $USD revenue takes a hit. In that case, the startup has to maintain its already ambitious VC-scale growth trajectory, but also has to grow faster than its currency depreciates. It’s stressful for the investor: they see their portcos’ $USD valuation crash, and are incentivized to push founders to grow at unrealistic rates.

This pressure is an immense psychological weight on founders, who can end up making aggressive, non-sustainable strategic decisions. Sadly, it can ruin what could’ve been a great company, but that is now burdened with an unattainable task. It can also severely bruise those who could have been fantastic founders.

To make things worse, Pakistani startups’ exit attractiveness is almost entirely dependent on their revenue. In Silicon Valley, the market is so liquid that a startup can grow fast, barely make money, and find exit options (secondaries, M&A) by pitching how valuable the data they’ve accumulated is.

That isn’t the case in Pakistan. The market for exits is scarce, and the only way to be attractive is to have strong revenue growth and healthy unit economics. Having those KPIs measured in a currency that’s way stronger than the currency your revenue is in is complicated.

RO insights: venture debt in local currency

For venture debt, the case to lend in local currency is salient since a depreciating currency immediately increases default risk.

Here’s how Mahmoud El-Zohairy, managing partner at Egypt’s Camel Ventures, explains it:

“If the companies we finance make money in Egyptian pounds, we’re going to lend in Egyptian pounds. Lending in USD to companies making money in a depreciating Egyptian pound increases their debt burden as well as their default risk. A depreciating pound means that their revenue continuously loses USD value. The vast majority of our LPs are Egyptian banks, so this strategy makes sense for us.”

Excerpt from On venture debt in Africa, originally published in The Realistic Optimist

Existing, $USD-denominated, Pakistani VCs are aware of that risk. Why did they raise $USD then?

Because it’s really hard to find local, Pakistani investors for a VC fund. This asset class is brand new here, and most investors fail to understand the illiquidity and uncertainty of a VC investment. Since the ecosystem is young, we also don’t have a ton of success proxies to point to.

On the other hand, international investors are more likely to understand the VC asset class, have seen home run returns in other markets, and are thus more likely to take a chance on a Pakistani VC.

Pakistani VCs that raised $USD didn’t make an unconscious strategic mistake, but contended with the lack of local options by raising money where they could, despite the currency caveat.

Where did you find your own, local investors?

First, we had to refine our investment thesis. As mentioned earlier, a “classic” VC investment strategy wouldn’t be palatable to local capital. We ended up creating a hybrid between a VC and a PE firm, with an emphasis on technology and export.

Source: Profit

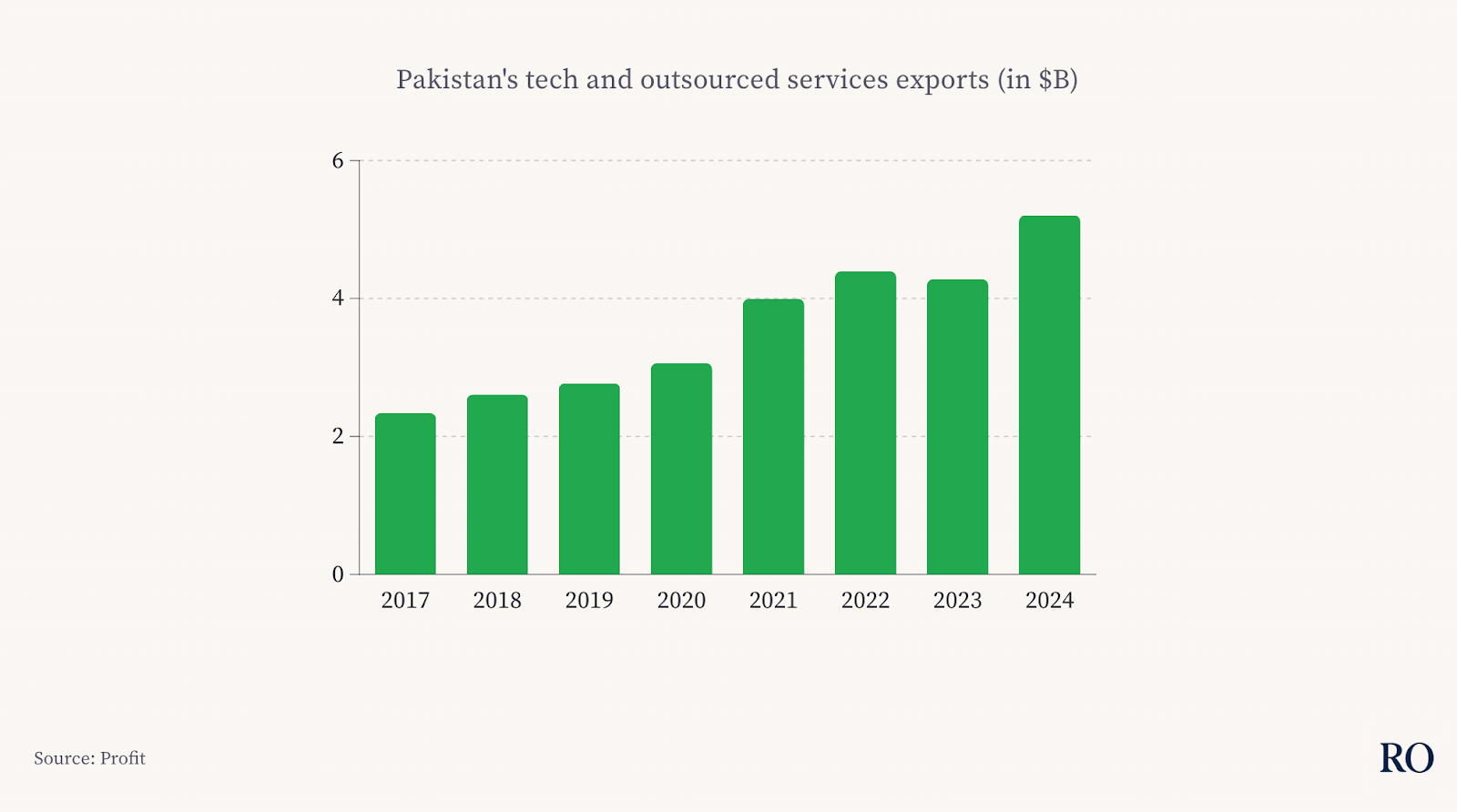

We invest in Pakistani companies that build advanced technology and sell that technology abroad. We’re also not dead-set on a pure “tech startup” play. We’ve invested in a couple of tech startups, but have also invested in service firms that provide advanced engineering for foreign clients. We chose the opposite of a spray-and-pray approach, building up a hyper-concentrated portfolio instead. We take an intensive operational role within the companies we invest in.

We’re flipping the script, if you will. We invest in Pakistani rupee but our portcos make revenue in stronger, foreign currencies.

We managed to sell that thesis to forward-looking, local family offices. We couldn’t really tap institutional investors such as DFIs and banks, because those require a track record, which we obviously initially lacked.

That leaves Pakistan-focused, B2C startups in a tough position then. What investment vehicle is best adapted to them?