Biography

Kayode Adeyinka is the co-founder and CEO of Gigmile, an African mobility fintech startup. Gigmile provides vehicle financing for gig workers, partnering with ride-hailing, e-commerce, and delivery platforms.

Gigmile launched in 2022 and has rapidly scaled through partnerships with asset providers (ex: automobile manufacturers) and financial institutions. Before founding Gigmile, Kayode was country manager at Jumia (one of Africa’s largest e-commerce companies) in Ghana and Nigeria,.

As of Q2 2025, Gigmile had raised a total $1.6 million in equity and over $16 million in debt, employs 100 people across Ghana and Nigeria, and operates in 10 cities.

How did your experience at Jumia inform how you’re building Gigmile?

I joined Jumia in 2014, during the early innings of African e-commerce. It was a different reality then. Many of the people we wanted to bring online didn’t even have email addresses, so we literally created accounts for them just so they could list their products.

I started out as a customer service manager, setting up that function from scratch, and then moved into growth, travelling across Nigeria, building sales teams, and convincing people to trust an online marketplace. Eventually, I moved to Ghana as country manager, where I had full responsibility for the business, including the P&L.

That journey showed me how to recognise the right time to scale, how to carefully hire, and how microeconomic realities (ex: cash-based earnings, low asset ownership, etc.) shaped last-mile logistics on the continent.

By the time I left Jumia, I’d gone from the very basics of setting up customer service to running an entire country operation. That dual experience, witnessing both the scrappy early challenges and the complexity of managing a full business, is what I brought into building Gigmile.

What challenges do African gig workers face that Gigmile wants to solve?

While many drivers are eager to work, they do not have vehicles (ie: income-generating assets) to do so.

At Jumia, whenever we had peak events like Black Friday or seasonal offers, the challenge wasn’t finding delivery workers, it was the fact that most of them didn’t own a motorcycle, a van, or even the right tools (ex: smartphones) to work. And for Jumia, traditional logistics companies like DHL or Aramex were far too expensive for last-mile delivery.

This customer segment remains deeply underserved, as traditional financial institutions are unwilling to provide financing. Drivers without collateral, credit histories, or even bank accounts are effectively invisible to the formal financial system. There is no pathway for them to access the kind of asset they needed to start working, even if they wanted to. That gap between the available labour force and available “work assets” financing was the challenge I kept seeing over and over again at Jumia.

Those reflections formed the genesis for Gigmile.

What kind of services does Gigmile offer? Do you go beyond vehicle financing?

We have always believed the solution had to be bigger than just vehicle financing.

Our core offering is a lease-to-own model aimed at gig workers. They pay daily for a period, usually between 18 to 24 months, and at the end of that period they own the vehicle. That’s our core business.

Their daily repayments provide them with a bundle of other services, such as maintenance, vehicle insurance, and driver insurance. This covers work disruptions like accidents, downtimes and thefts. We also help drivers with the necessary licenses they need to work as a gig worker.

Once the driver has the resources to work, we connect them to companies that need them. Through our partnerships with companies like Bolt, Jumia, and Yango, we directly onboard riders and make sure they’re earning from day one.

As they build up a payment history and eventually own their vehicle, we are able to extend other services like micro-credit, which allows them to finance other things (opening a shop, buying another vehicle, or supporting their family). Over time, the goal is to create a financial pathway that goes beyond the first vehicle and helps them build financial resilience.

Can you share some traction numbers?

Today we have more than 8,000 gig workers, with about 6,200 of them currently active. Around 1,500 have already finished paying for their assets and own those vehicles outright. Of these 8,000 gig workers, nearly 65% of them operate in the unorganised sector offering ad-hoc ride hailing services (ie: your classic moto taxi), and 35% of them are engaged with organised platforms such as Jumia, Bolt, or Uber.

As of Q2 2025, Gigmile had raised a total $1.6 million in equity and over $16 million in debt, employs 100 people across Ghana and Nigeria, operates in 10 cities, and achieved its first profitable quarter in Q2 of this year. The bulk of the debt has been raised from top global original equipment manufacturers (OEMs), with current partnerships including Yamaha, TVS, Bajaj, and Hero, four of the five largest light vehicle manufacturers worldwide.

How do you make money, and how do you expect that to evolve?

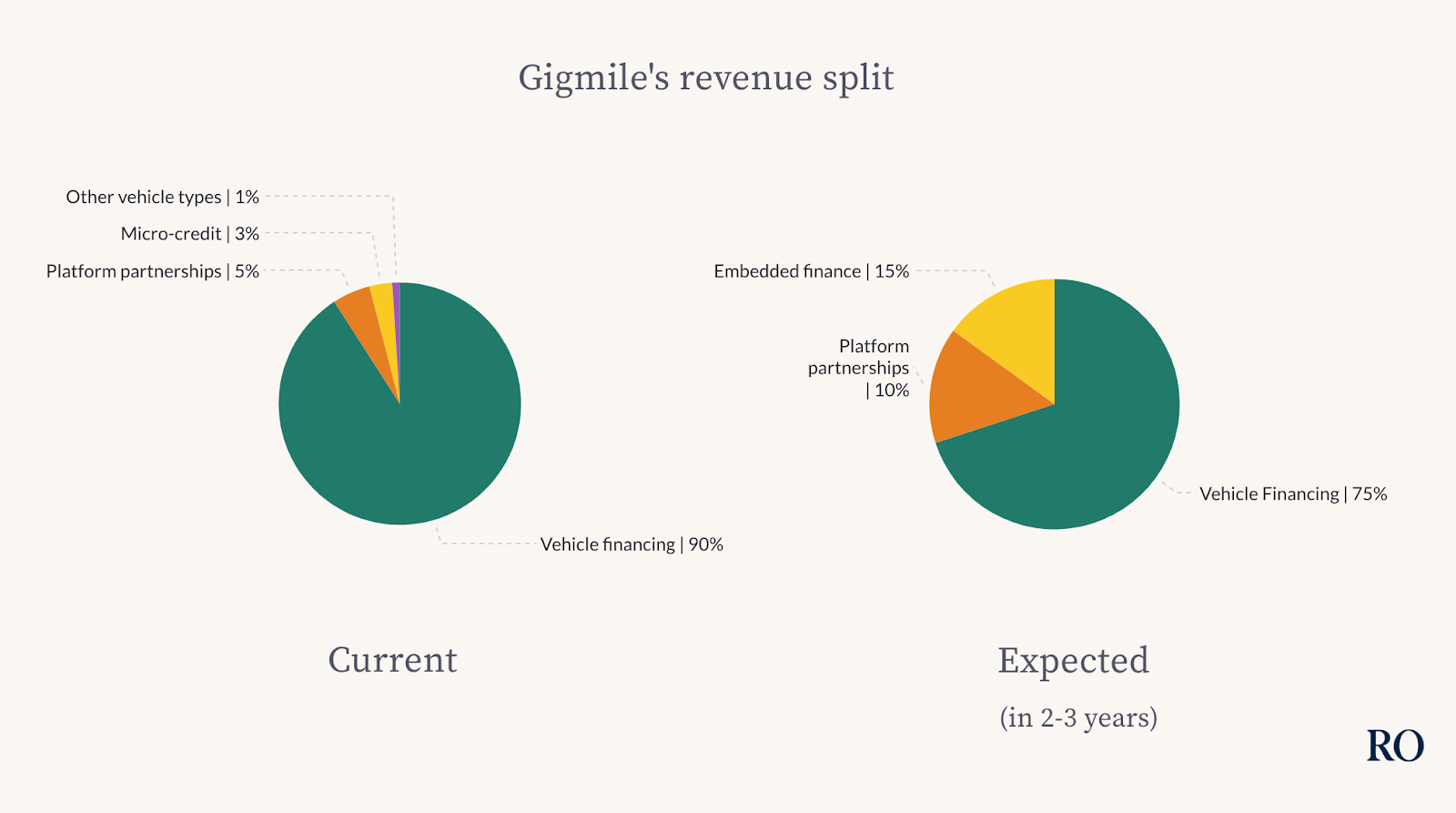

Today, about 90–93% of our revenue comes from our lease-to-own arm, where riders pay daily over 18–24 months until they own the asset. We lease vehicles at terms that generate returns above our purchase and operating costs.

Around 5% comes from partnerships with platforms like Bolt, Jumia, and Mano. In these cases, we earn a revenue share of roughly 3–5% of the total order value that the platform itself takes from a delivery driver. Platforms are willing to revenue-share because Gigmile allows them to plug-and-play an existing network of drivers in a given area, instead of them having to build it up from scratch.

For instance, we manage end-to-end logistics for Mano, a grocery delivery startup operating in Lagos and Abuja. Rather than them worrying about sourcing drivers or vehicles, they simply tell us what they need, and we provide it.

The remaining 2% comes from micro-credit, which is still very much in pilot.

Looking ahead, vehicle financing will remain the biggest revenue channel, but we expect it to come down to around 75% over the next three years as platform revenues grow and micro-credit/other financial services scale up. We also plan to expand the range of vehicles we finance beyond motorcycles and three-wheelers, into cars and minibuses.

How does Gigmile itself finance the vehicles it offers on the lease-to-own plan?

We work hand in hand with the automobile original equipment manufacturers (OEMs).

In developing markets, auto-OEMs usually have a financing arm that works with buyers to set up a financing plan for their vehicle. Companies like Bajaj and TVS do this in India. But in Africa, OEM-led financial infrastructure for automobile purchases doesn’t exist. We are filling that gap.

We have begun partnerships with a few of the OEMs. This financing model is either a sub-lease model (where we lease the vehicles from the auto-OEMs and lease them out to gig workers) or a direct lease (where we lease out vehicles we have purchased from OEMs outright).

How do you underwrite gig workers?

Our underwriting process had to be built from scratch because traditional financial institutions wouldn’t touch this customer base. These gig workers often don’t have collateral, credit history, or even a bank account, so the usual credit checks don't apply.

We started with something simple back in 2022, just five basic questions (a mix of behavioural and psychometric questions) to gauge whether someone could and would pay. By 2023, we had grown that to around 16 checks. Today, our underwriting model includes over 70 different inputs.

We assess two key factors: willingness to pay and ability to pay.

Each of those has layers beneath it. We look at guarantors, we collect social proof, and we verify documents in alternative ways. We’ve also built technology to make this process scalable, from tagging locations, to verifying guarantors quickly, to tracking repayment patterns in real time. (ED: this is also the case in India. Financial institutions will look at social proof by interviewing and talking to community members, family members, and distant relatives to measure a person's creditworthiness and ability to pay.)

We design our pricing to match our customers’ microeconomic realities. We don’t let repayments exceed 33% of a gig worker’s daily expected earnings, ensuring they can meet their payment obligations but also take some money home.

RO insights: credit scoring unbanked customers

Startups extending credit to first-time borrowers often face a credit scoring challenge: they have scarce data available to decide whether to lend to the person or not.

To remediate, startups mix different methods. One is to start by lending tiny amounts, and let the borrower gradually build an in-house credit score. Another is to use a series of questions, to gauge the borrower’s personality and extrapolate their propensity to repay.

Here’s how Halima Iqbal, co-founder of Pakistani fintech Oraan, explains how they go about it:

“Pakistan doesn’t have a centralized database of identities, such as Aadhaar in India. We’ve had to build our database and individual credit scores from scratch.

Here comes the hard part: how do you underwrite someone with no document proving either asset or income? It involves a lot of creativity and trial and error.

We use behavioral data as a substitute for the non-existent financial data we have on applicants. We have questionnaires that try to determine the person’s personality and their propensity to pay back. We can use how a person has organized their contacts and photos in their phone to determine whether they’re organized or not.”

Excerpts from Oraan: digitizing Pakistani credit unions originally published in The Realistic Optimist

What counter-intuitive lessons have you learned from how gig workers operate?

Some of our best-paying customers come from the informal motorcycle taxi sector rather than organised platforms. You would think platforms, with their structure and data, would give more stability. But in reality, workers using them face fluctuations due to platform-related injections like surge pricing, seasonal offers, peak hour traffic, etc.

On the other hand, informal motorcycle taxi drivers often cover the same areas, and have a ballpark idea of how many passengers they’ll carry in a day. That consistency makes them more reliable in repayments.

Another pattern we’ve seen is that drivers who have family responsibilities tend to manage repayments better than single drivers. The sense of responsibility translates into repayment discipline. We’ve also learned that geography matters, some areas are at higher risk than others because of local economic conditions or driver density, which drives down average earnings.

Gigmile is a capital-intensive endeavor. How have you set up the company’s finances?

With motorcycles costing around $1,000 and three-wheelers about $2,200, scaling to over 7,000 vehicles adds up quickly. From day one, we have been deliberate and frugal in how we construct our capital stack, knowing where, when, and how to unlock the right capital for scale while keeping FX risk minimal.

To date, we have raised more than $16 million in debt, but more importantly, we continue to build a robust and diversified capital structure. This includes partnerships with OEMs, traditional financial institutions, and government-backed financing programs such as our current collaboration with CREDICORP.

This approach ensures we can scale sustainably while aligning our financing model with the realities of our market.

Are there any foreign startups Gigmile is inspired by, and what are you doing the same or differently?

When we first started Gigmile, it wasn’t because we looked at another company and said, ‘let’s replicate this.’ It began almost accidentally, as a social experiment of sorts. It grew into a business because the need was so obvious. As we built the model, we found inspiration in a few international players. In Mexico, there’s Mottu which has a wide offering, in India there’s Zypp, which focuses on EVs. They all share some similarities with what we’re doing.

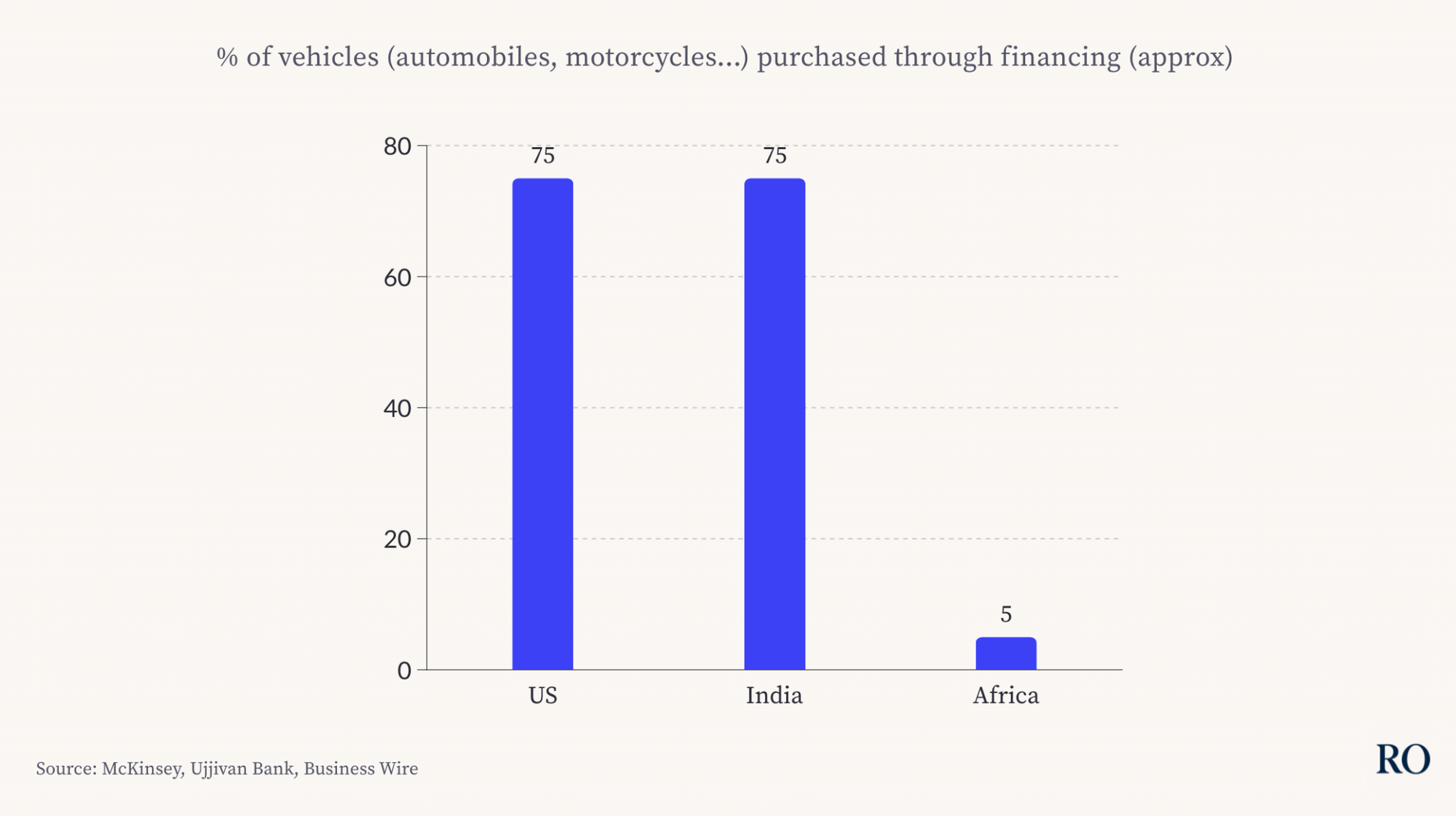

What’s different for us is how we’ve adapted this to African realities. In India, about 75% of motorcycles are financed through vehicle financing. In the U.S., between 70-80% of vehicles are purchased via financing. But in Africa, that number is way lower, possibly in the single digits. That gap is why a company like Gigmile needs to exist.

We are building for markets where traditional financing options are missing, infrastructure is weak, and informal motorcycle taxis are just as important as platform-based work. So while the international examples gave us ideas, our underwriting model, our partnerships with OEMs, and our focus on solving for structural gaps are specific to this continent. We’re not just providing vehicles, we are creating a financing ecosystem that fits the realities here.

Sources: McKinsey, Ujjivan Bank, Business Wire

What does the future of Gigmile look like?

First, on international expansion, we plan to enter new markets in Francophone Africa and one or two countries in East Africa. Some pilots have already begun and we expect to be fully operational in those markets within 18 months. The model won’t change, we’ll still be connecting gig workers to vehicle financing and linking them with platforms.

The problem we are solving is not unique to Africa, it exists across other emerging markets such as Bangladesh, the Philippines, and beyond. In the coming years, there is strong potential to expand in these directions and replicate our model where similar systemic challenges exist.

Second, in terms of product mix, our business today is still largely driven by vehicle financing, which accounts for roughly 90–93% of our revenue. Looking ahead, we are expanding into embedded financial services, including savings, bill payments, and micro-credit, with the goal of making our Gamma Mobility app a full-fledged financial companion for gig workers.

We have also started expanding into the personal segment (our first foray away from the gig worker segment), extending our lease-to-own offer on scooters for salaried workers using them for personal commuting.

In terms of revenue mix, (as mentioned above) vehicle financing will remain our largest contributor, though its share is expected to decline to around 75% as we diversify. Embedded finance will account for roughly 15%, while platform partnerships (where we directly supply riders to platforms), will contribute the remaining 10%.

Gigmile’s Gamma Mobility app

RO insights: becoming African gig workers' superapp

Gig workers, in Africa and elsewhere, generally lack adequate digital financial services, due to their lower socio-economic status. Fintechs and banks may prefer to focus on the higher-earning, more stable middle class.

This creates a gap in the market, which startups are filling. Compared to other unbanked customers, gig workers have a semi-recurrent, provable revenue source that startups can use to underwrite credit. VC-backed startups being incentivized to go big or go home, the goal often isn’t to stop at credit, but become gig workers’ financial companions.

Renda, a Nigerian startup, is building a super app for delivery drivers. It offers an interesting product, extending credit for maintenance work. Here’s how Renda co-founder Ope Onaboye explains:

“Scale isn’t just for our delivery partners. It’s for individuals and businesses operating in the logistics and mobility industry. Although the product isn’t public yet, it's live.

Scale is deeper than a simple credit product. It’s a superapp for delivery drivers, where they can access a network of mechanics, fuel stations, spare part sellers, health insurance providers, CNG conversion mechanics…

Drivers can buy services from the app on credit. Renda pays the service provider the full price directly and then takes care of collections on the driver side. We’ve spent the past few months running a pilot, funding it internally to better understand our customers’ risk profiles and operational dynamics.

Now, with insights from that phase, we're working with finance partners to help us scale and grow the product sustainably.”

Excerpt from Renda: digitizing African logistics, originally published in The Realistic Optimist

What do foreign investors often get wrong about the Nigerian startup scene?

One of the recurring misconceptions foreign investors bring to the Nigerian and African startup landscape is the belief that the Silicon Valley playbook can be applied here, wholesale. While well-intentioned, this often overlooks the need to adapt strategies to the unique realities and systemic challenges of our markets.

The challenges we face in Africa are not just business inefficiencies; they are deep, systemic, and interwoven “wicked problems.” Many investors gravitate toward asset-light SaaS businesses, but the reality is starkly different: our barriers are infrastructural, not merely digital. We lack reliable roads, efficient transport systems, and even access to the basic tools that enable productivity. Funding pure software solutions often means addressing surface-level symptoms while leaving the root causes untouched. To create real impact, you must engage with the hard, infrastructure-heavy problems that define everyday life here.

Nigeria has over 200 million people, and Africa has more than a billion. These numbers present an opportunity as long as purchasing power and per capita GDP continue to grow. The real opportunity meanwhile is not in seeking to flip many billion-dollar valuations. These will exist, but the major opportunity in Africa is in building hundreds of resilient, $100–300 million businesses that address everyday, systemic needs. That’s where the real impact and sustainable returns lie.

And then there’s the focus on fintech. Of course, payments matter, and companies that solve with stablecoins and AI are important, but there are tons of other critical problems in transportation, logistics, agriculture, and energy that need solving. When capital keeps flowing only into trendy categories, startups that are tackling real infrastructure gaps get overlooked.

For me, what foreign investors often miss is that capital here has to be patient, and aligned with the local realities. If you come in expecting Silicon Valley-style multiples without solving Africa’s systemic issues, you’ll almost always be disappointed.

The Realistic Optimist’s work is provided for informational purposes only and should not be construed as legal, business, investment, or tax advice.